Goods and Services Tax (GST) in New Zealand is a broad-based consumption tax applied to most goods and services, currently at a rate of 15%. While seemingly straightforward, its application to real estate transactions in New Zealand can be complex, impacting everyone from individual homeowners to large-scale developers and commercial investors. This article delves into the nuances of GST in various real estate scenarios, including commercial properties, new builds, rentals, leases, and the role of trusts.

The Fundamentals: When Does GST Apply to Real Estate?

GST generally applies to the sale and purchase of “taxable supplies” of land and buildings. A key determinant is whether the vendor (seller) is GST-registered and whether the property is being used to make taxable supplies.

Key Principle: If both the vendor and purchaser are GST-registered and the property is being used to make taxable supplies, the transaction can often be zero-rated for GST, meaning no GST is physically paid on settlement. However, specific conditions must be met.

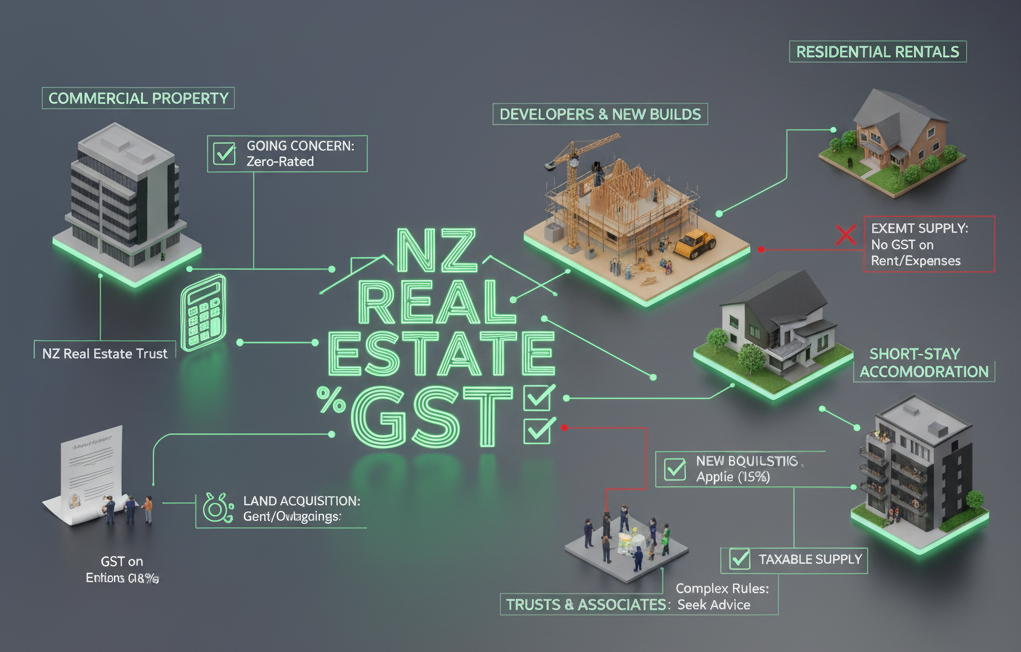

Commercial Buildings: The “Going Concern” Exemption

The sale and purchase of commercial buildings are prime examples where GST becomes a significant consideration.

- Standard Commercial Sale: If a GST-registered vendor sells a commercial building to a GST-registered purchaser, and the property is used by the vendor to make taxable supplies (e.g., renting it out to commercial tenants), the transaction can often be zero-rated for GST if certain conditions are met. This means no GST is added to the purchase price, and no GST is claimed back by the purchaser. The property must be sold as a “going concern.”

- “Going Concern” Defined: For a supply of commercial property to be zero-rated as a “going concern,” the vendor must supply all things necessary for the purchaser to continue the taxable activity. In the context of a commercial building with existing tenants, this typically means the building itself and the existing leases/tenancy agreements. The purchaser must also intend to carry on the same (or a similar) taxable activity.

- Implications of Not Meeting “Going Concern” Criteria: If the “going concern” criteria are not met (e.g., the vendor is GST-registered but the purchaser is not, or the property is sold vacant and the purchaser does not intend to lease it out for taxable purposes), then GST at 15% would typically be added to the purchase price, and the purchaser would either have to pay this or factor it into their claiming back of GST if they become registered.

- Buyer Not GST Registered: If a GST-registered vendor sells a commercial property to a non-GST-registered purchaser, GST at 15% will be added to the purchase price.

Developers and New Builds: A Central Role for GST

Developers operate squarely within the GST regime, as their core business involves making taxable supplies of new residential or commercial properties.

- Land Acquisition: When a developer acquires land for development, if the vendor is GST-registered and the land was used to make taxable supplies, the acquisition can often be zero-rated. Otherwise, GST might be added, which the developer can typically claim back if they are GST-registered and intend to use the land for taxable supplies.

- Construction Costs: Developers can claim back GST paid on all construction costs, materials, and services (e.g., architect fees, builder invoices) incurred in the development process, provided they are GST-registered.

- Sale of New Builds:

- New Residential Properties: The sale of a new residential property by a GST-registered developer is subject to GST at 15%. This GST is included in the advertised sale price. Purchasers of new residential homes are typically not GST-registered, so they pay the GST as part of the purchase price.

- New Commercial Properties: Similar to existing commercial properties, the sale of a new commercial property by a GST-registered developer to a GST-registered purchaser can often be zero-rated if sold as a “going concern” (e.g., with an existing commercial tenant in place) and the purchaser intends to continue the taxable activity. Otherwise, GST at 15% applies.

Rental Properties: Residential vs. Commercial

The GST treatment of rental income varies significantly depending on the type of property.

- Residential Rentals: The supply of residential accommodation for long-term rental (e.g., a standard residential tenancy agreement) is an exempt supply for GST purposes. This means landlords of residential properties generally cannot register for GST in relation to their rental income, nor can they claim back GST on expenses related to these properties (e.g., maintenance, property management fees).

- Exception: Short-Stay Accommodation: If a property is rented out as short-stay accommodation (e.g., Airbnb, motels, serviced apartments), this is generally considered a taxable supply, and the owner would typically need to register for GST if their turnover exceeds the threshold.

- Commercial Rentals: The supply of commercial property for rent is generally a taxable supply. Landlords of commercial properties typically need to be GST-registered if their gross income from all taxable activities (including commercial rent) exceeds the annual GST registration threshold ($60,000). Once registered, they must charge GST on the rent and can claim back GST on all associated expenses.

Leases: GST on Rent and Outgoings

For commercial leases, GST is a standard component.

- Rent: The landlord, if GST-registered, will charge GST on top of the base rent. The tenant, if also GST-registered, can typically claim this GST back.

- Outgoings: Any outgoings (e.g., rates, insurance, body corporate fees) that are passed through to the tenant under the lease agreement and represent a recovery of the landlord’s expenses will also typically have GST applied to them by the landlord.

Trusts and Real Estate

Trusts are common vehicles for holding real estate in New Zealand, and their GST obligations mirror those of individuals or companies depending on their activities.

- Residential Rental Trust: If a trust holds residential rental properties for long-term lease, it generally cannot register for GST as residential rent is an exempt supply.

- Commercial Property Trust: If a trust holds commercial properties and derives commercial rental income, it would likely need to register for GST if its turnover exceeds the threshold, similar to an individual or company landlord.

- Development Trust: A trust engaged in property development would be treated as a developer for GST purposes, with the associated obligations and entitlements to claim GST on costs and charge GST on sales.

- GST Grouping: It’s possible for multiple trusts or entities under common control to form a GST group, which can simplify GST reporting and intra-group transactions.

Common GST Pitfalls and Considerations

- Changing Use: If a property’s use changes (e.g., from a commercial rental to a private residence, or vice-versa), adjustments may be required to previously claimed or accounted for GST. This is known as an “adjustment for change in use.”

- GST Registration Threshold: The current GST registration threshold is $60,000 of taxable supplies in a 12-month period. Businesses (including those involved in real estate) whose turnover exceeds this must register for GST.

- Zero-Rating Requirements: Strict conditions apply to zero-rating land transactions. Ensure all parties are GST-registered, the property is used for making taxable supplies, and the intention to continue the taxable activity is clearly documented. Legal and accounting advice is crucial here.

- Sale of Bare Land: The sale of bare land can be subject to GST if the vendor is GST-registered and acquired the land with the intention of making taxable supplies (e.g., as part of a development project).

- Associated Persons: Special rules apply when transacting with “associated persons” (e.g., family members, related companies), which can impact market value considerations for GST purposes.

GST in New Zealand real estate is a multifaceted area requiring careful consideration and professional advice. The distinctions between residential and commercial properties, the specific activities of developers, the intricacies of “going concern” provisions, and the various structures used to hold property all have significant GST implications. Engaging with experienced property lawyers and tax advisors is essential to ensure compliance, mitigate risks, and optimize financial outcomes in New Zealand’s dynamic property market.

Disclaimer:

The information provided in this article is general in nature and should not be considered as legal, financial, or professional advice. Buyers/sellers are strongly encouraged to seek independent legal and/or financial advice from qualified professionals before making any decisions related to property transactions.

Join The Discussion